The first MACSE auction, held in late September 2025, allocated the full 10 GWh of capacity on offer in Central, Southern and island bidding zones, under 15-year, fixed-price tolling agreements. The auction functioned on a pay-as-bid basis, with final awarded prices averaging just below 13 kEUR/MWh/year, according to TSO Terna, almost three times lower than the ceiling price of 37 kEUR/MWh/year. Average capacity of awarded projects was 125 MW and duration averaged at 6.7 hours, with all awarded assets being above 6 hours. Enel emerged as the dominant player, securing over half of the available capacity, including the 574 MW Brindisi 3 site, among the biggest BESS assets in Europe. Other successful bidders included ZE Energy, BW ESS, Greenvolt, Whysol, NatPower, and Eni Plenitude, with ZE Energy’s 8.4-hour system in Sessa Aurunca representing the longest-duration project awarded.

The results highlight that amid the fierce competition, some developers exhibited a clear willingness to sacrifice potentially much higher merchant upside in exchange for guaranteed returns. This was also shown in the concentration of higher duration assets among the winners, due to merchant-equivalent revenues for these projects being significantly closer to MACSE awarded bid prices than those of lower duration assets.

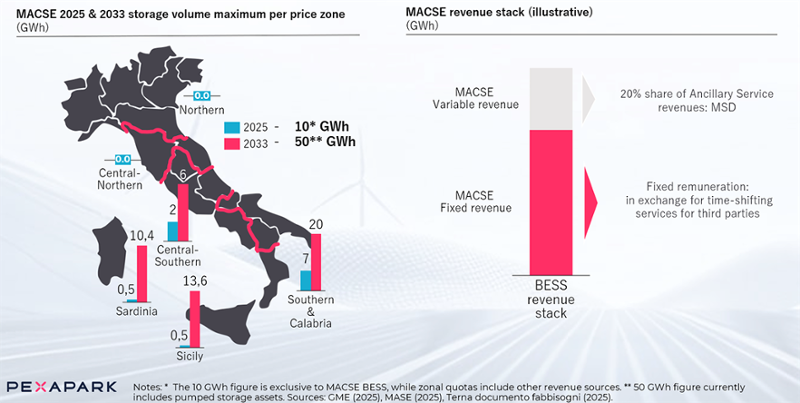

MACSE auction offers guaranteed revenues for BESS

Source: Pexapark

The MACSE mechanism functions as a tolling contract, meaning project revenues are effectively “swapped”: the awarded assets give up exposure to wholesale price fluctuations and, in return, receive monthly payments from TSO Terna corresponding to their bid, as well as a minority portion of ancillary service revenues.

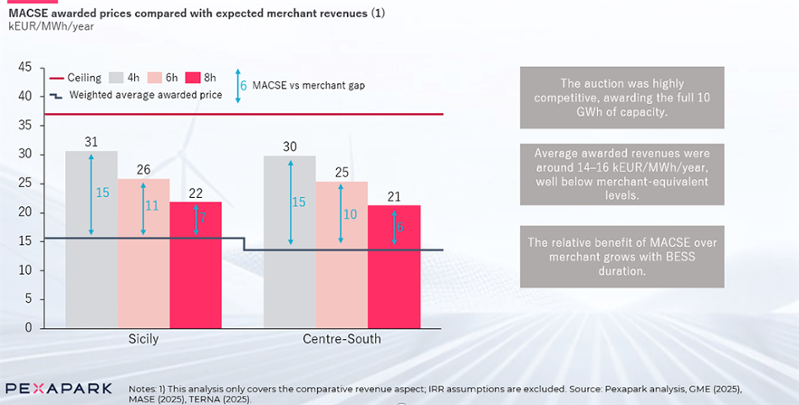

However, the winning bids in the first MACSE auction showed exceptionally low prices, cutting expected revenues to a significant degree in order to secure long-term contracts. According to Terna’s published MACSE results, awarded projects in Sicily and the Centre-South zones achieved weighted average prices of 15.8 kEUR/MWh/year and 14.5 kEUR/MWh/year respectively, 40% less than the 37 kEUR/MWh/year bid ceiling.

A key factor in the low clearing prices was Enel’s dominant position and the company’s ability to leverage economies of scale. Among its winning projects, Brindisi 3, located in a decommissioned power plant, benefited from existing grid connections and land rights, reducing CAPEX as well as costly permitting and connection hurdles. Market participants told Pexapark that Enel’s size likely enabled it to secure financing at lower cost, allowing the company to lower its bid further.

Pexapark analysed the trade-off between revenues under the MACSE scheme and merchant revenues over the same contract duration, here focusing solely on revenue projections and excluding cost and IRR considerations. The analysis shows that shorter-duration assets would have given up considerable upside potential in exchange for long-term revenue certainty.

However, merchant revenues are highly volatile: in best-case scenarios (P10), they can reach up to almost twice the average value across simulated scenarios. On the other hand, in adverse (P90) cases, these can be more than 60% lower than expected, converging closer to the fixed MACSE payments. The expected revenue spread narrows as storage duration increases: 6-hour and 8-hour systems show smaller relative differences between the two revenue models. It is likely that developers placed strong emphasis on the value of the merchant tail beyond the 15-year contract period to offset the low fixed revenues.

MACSE BESS Auction winners forego merchant revenue upside in exchange for long term stability

Source: Paxapark

The analysis clearly shows that 6- to 8-hour duration BESS display a much narrower gap between expected merchant revenues and MACSE remuneration, estimated at around 10–11 k€/MWh/year for 6-hour and 6–7 k€/MWh/year for 8-hour systems. This makes them well positioned to benefit from the scheme’s fixed payments while giving up only a limited portion of their potential market upside.

In contrast, shorter-duration assets, such as 4-hour batteries, would face a far steeper trade-off: merchant benchmarks in Sicily and the Centre-South sit roughly twice as high as the awarded MACSE prices, making participation less attractive for those configurations. This means that while short-duration systems trade away substantial upside, longer assets can achieve stability with a more modest revenue compromise.

BESS revenue stack and zonal dynamics

Pexapark’s modelling of the Italian BESS revenue stack for the MACSE bidding zones shows a strong reliance on ancillary service markets (MSD), which depending on the specific zone and the asset optimisation, can generate more than half of total revenues. By contrast, returns from the Day-ahead market are considerably lower and largely dependent on short-term price volatility, while the Intraday market contributes only marginally, reflecting its limited trading volumes and narrower spreads. Italian Day-ahead spreads have narrowed sharply since the volatility peak of 2022, when a hypothetical 4-hour battery could have captured on average 142 EUR/MWh in southern zones; by mid-2025, these spreads averaged around 88 EUR/MWh per day.

Southern and island bidding zones offer highest Day ahead price spreads for 4-h BESS

Source: Pexapark

The MSD now forms the backbone of BESS profitability, offering higher revenues than Day-ahead trading despite lower volumes on offer. Between January and May 2025, up-regulation prices averaged 250 EUR/MWh in the Centre-South and 320 EUR/MWh in Sicily, several times above Day-ahead levels. However, these same southern zones remain among the most volatile and prone to congestion and curtailment, making such elevated returns uncertain over time. MACSE’s fixed-revenue model helps mitigate these risks by stabilising cash flows, appealing to developers seeking more predictable returns.

The MACSE auction proved that developers are ready to compress margins to secure 15-year fixed revenues, even when this means reducing potential merchant earnings. This outcome underscores a growing divide in Italy’s BESS market: long-duration systems have found their niche within MACSE, where stable, long-term contracts best reward their profile, while shorter-duration assets remain better suited to the merchant market, where flexibility and volatility can still deliver superior returns.

Industry observers are already calling to cap the size of individual participant portfolios in future MACSE rounds, meaning these could see higher clearing prices and a more balanced competitive landscape, reducing the risk of bids falling to unsustainable levels.