On 2–3 September 2025 Russian and Chinese leaders announced a legally binding memorandum of understanding (MoU) to construct the Power of Siberia 2 pipeline (PoS2) — a proposed 50 bcm/year route from Russia to China via Mongolia — and agreed modest increases to flows on the existing Power of Siberia (PoS1) and Far East routes. While the ceremony is politically significant, key commercial terms — notably price formula, offtake final investment decisions (FIDs) and SPA— remain unresolved.

That distinction matters: a MoU preserves the geopolitical option and begins preparatory work, but does not guarantee PoS2 will be delivered on a timetable that materially changes global gas balances in the 2030s.

Lessons from PoS1

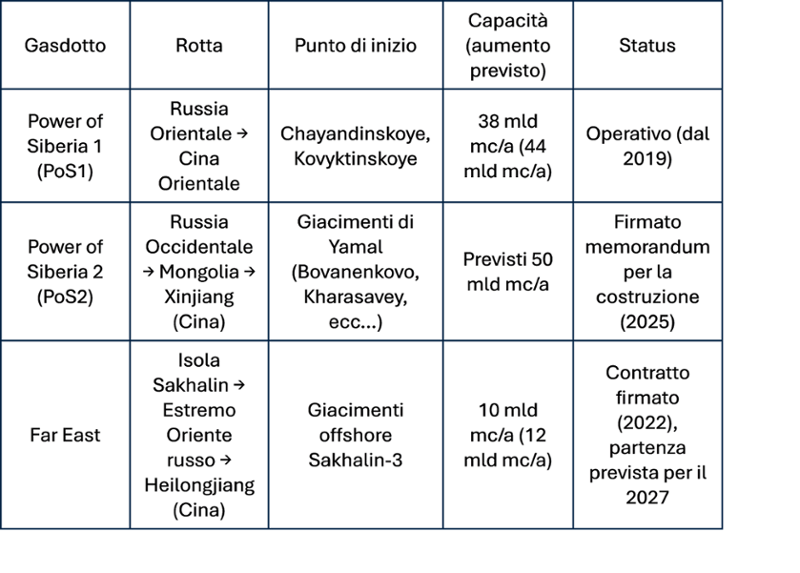

Russia is methodically expanding its pipeline gas export infrastructure to China through three principal routes, signalling a long-term strategic pivot eastward. The operational Power of Siberia 1 (PoS1) pipeline — with a capacity of 38 bcm/year (scheduled to expand to 44 bcm/year) — serves as the foundational corridor. It will be complemented by the Far East route (currently 10 bcm/year, expected to reach 12 bcm/year and enter service around 2027), which is under development. The ambitious Power of Siberia 2 (PoS2), with a planned capacity of 50 bcm/year, represents the largest potential growth vector but remains at an early stage, with only a binding construction MoU signed as of late 2025.

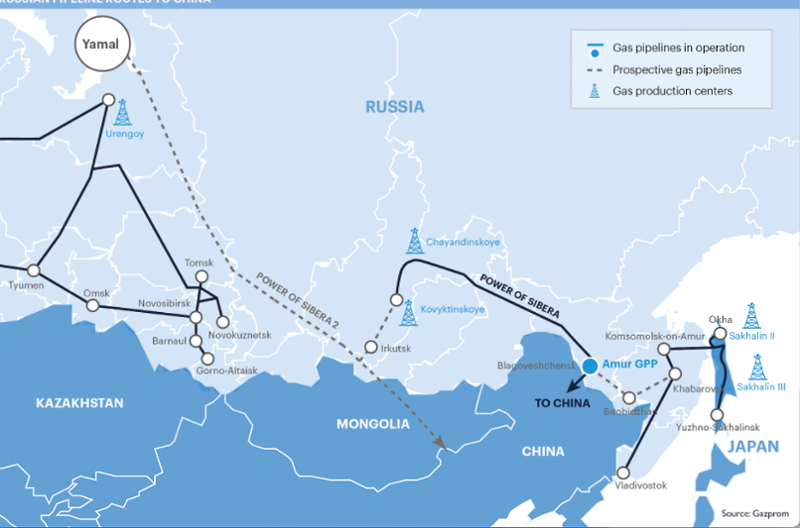

Main Russia-China pipeline

Source: ICIS

PoS1 is the landmark project that converted decade-long political discussions into a functioning supply corridor. Gazprom signed the SPA with CNPC in 2014, commissioning began in late 2019, and PoS1 gradually ramped to contracted volumes over subsequent years. That steady ramp demonstrates the long lead times required for mega inter-border pipeline projects. PoS1’s multi-year ramp-up underscores that political will alone does not eliminate engineering, capex and pricing hurdles. The same constraints will shape PoS2, which faces larger technical and commercial complexity, including the challenges of developing northern Yamal fields, long overland transit across Mongolia, and substantially higher upfront capital requirements.

Russian Pipeline Routes to China

Source: Gazprom

Risk of Chinese gas oversupply

China’s supply-side dynamics raise a considerable risk of oversupply around 2026–2030 — precisely the period when PoS2 would need to prove incremental offtake.

ICIS estimates that Chinese buyers signed a total of 56 mtpa of long-term LNG contracts in 2021–23. A large share of those volumes is scheduled to begin deliveries in 2026–2028, creating a delivery-timing cluster.

Moreover, the structure of many new contracts is more flexible — most are FOB-based. This flexibility gives Chinese buyers levers to defer, reroute, or resell cargoes if domestic market conditions weaken. Beijing and Chinese firms can also reduce or delay pipeline take-or-pay exposure where spot prices and domestic policy justify such choices. In practice, PoS2’s commerciality will be judged against an enlarged menu of lower-risk supply and pricing options.

Demand challenges

China’s gas demand has softened relative to legacy projections due to structural changes, limiting appetite for a single large-volume supply source.

Property construction and associated investment — historically a major driver of industrial output and energy use — has been weak since 2021 and remained a drag through the last two years. Reduced construction activity depresses industrial gas demand, particularly for gas-intensive outputs. Output of flat glass and crude steel — both key gas-consuming sectors and central to coal-to-gas transition policies — fell by 4.1% and 9.2% year-on-year so far in 2025, respectively. Although emerging industries such as electric vehicles and industrial robotics are expanding rapidly, their energy needs are met primarily through electricity rather than gas. As such, they cannot compensate for the property-driven decline in gas-intensive sectors, leaving the base-case gas demand trajectory lower than in previous cycles.

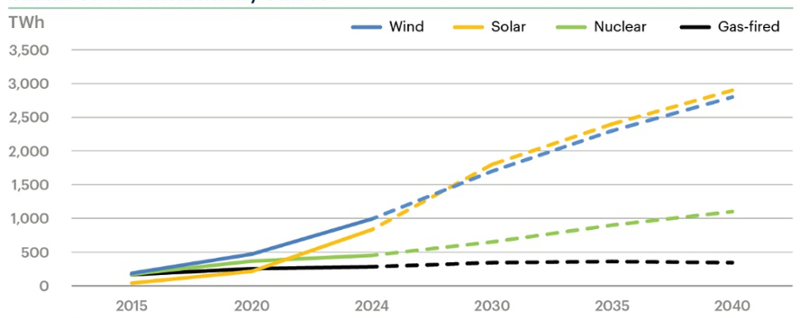

China Power Generation by source

Source: ICIS, NBS

At the same time, the rapid expansion of alternative energy sources is likely to further suppress gas demand. China remains the world’s largest builder of clean energy: over the past five years wind, solar and nuclear generation have all grown strongly. Wind and solar generation nearly tripled, rising from roughly 730 TWh in 2020 to over 1,820 TWh in 2024. Nuclear output also advanced steadily, with multiple reactors under construction. ICIS expects these three sources combined to reach c. 5,600 TWh by 2035 — almost triple the 2024 level. Such expansion will erode gas competitiveness, particularly in the context of China’s carbon-peaking commitment by 2030.

Impact assessment

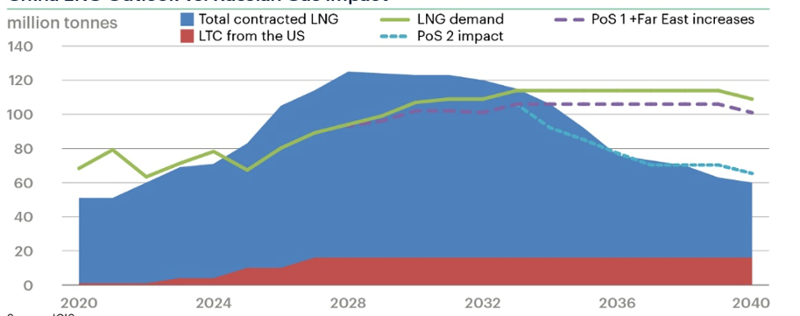

ICIS currently assesses that incremental supply from confirmed expansions of PoS1 and the Far East pipeline will ramp up after 2027. This combined volume — equivalent to approximately 5.7 mtpa or about 80 standard LNG cargoes per year — will provide China with a substantial and stable source of pipeline gas, enhancing energy security. The outlook for PoS2 remains highly uncertain: the absence of a firm SPA and a final investment decision creates significant timing risk, and gas flows are unlikely to commence before 2033.

China LNG outlook vs Russian Gas Impact

Fonte: ICIS

ICIS does not expect PoS2 to progress rapidly in the near term. However, should PoS2 ultimately be delivered, China’s LNG market would be profoundly affected. At full capacity, PoS2’s 50 bcm/year could displace up to c. 30% of China’s projected LNG imports by the mid-2030s — roughly 36 million tonnes annually. Although the country is likely to be over-contracted in the near term, ICIS estimates it could become under-contracted after 2030 if current contracted volumes are left unchanged, thereby creating demand for new supplies.

This shift would not only diversify China’s import mix but also rebalance global LNG trade, alleviating anticipated market tightness in the mid-2030s and exerting downward pressure on long-term contract prices.