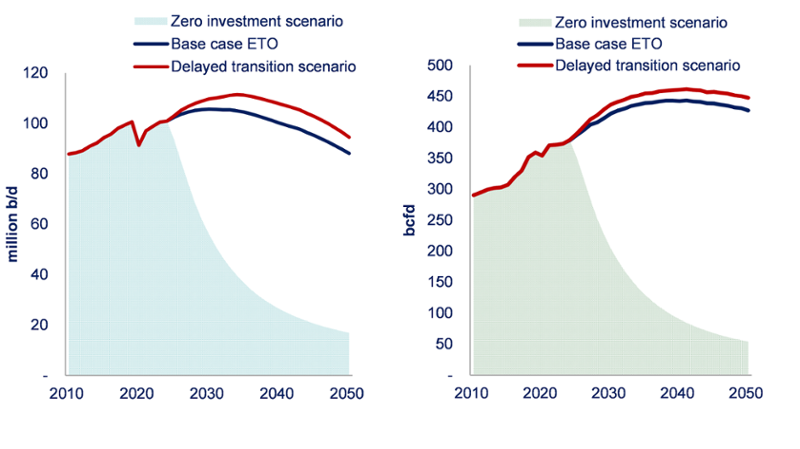

The world is edging towards a slow-paced energy transition, with fossil fuels remaining cheaper and more accessible than many lower-carbon alternatives. In Wood Mackenzie's base case, the world is on a 2.5°C pathway, with liquids demand slowly peaking early next decade around 106 million barrels per day (b/d) and gas a decade later at over 440 billion cubic feet per day (bcfd).

However, a delayed transition scenario, assuming a five-year delay to global decarbonisation efforts, would result in a 3°C pathway requiring 5% more oil and gas supply. In this delayed scenario, liquids demand would average 6% higher than the base case to 2050, while gas demand would be 3% higher. Meeting this increased demand while managing existing field declines would pose significant challenges for the industry, particularly in the medium to long term.

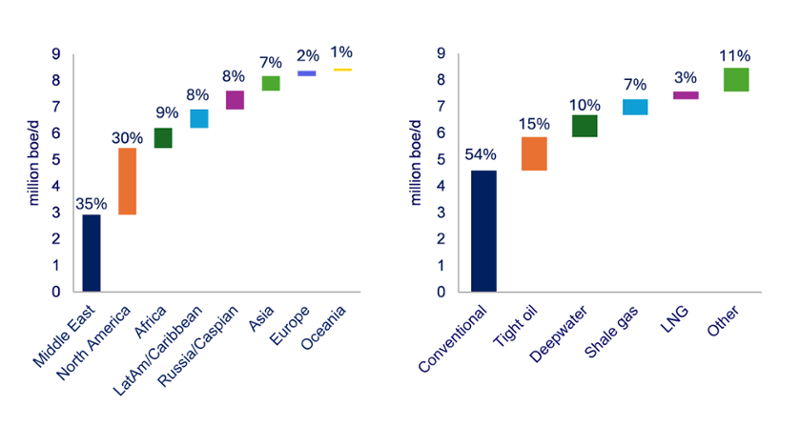

The liquids supply increment is roughly equivalent to the volume of a new US Permian basin; additional gas supply is on a par with current production of Australia. It would mean investment would have to increase materially, but more spending would put significant pressure on the supply chain, parts of which are already running near capacity.

In this Horizons we dig a little deeper into the key issues a delayed transition scenario would bring for the upstream sector.

Liquids demand scenarios Gas demand scenarios

Source: Wood Mackenzie Energy Markets Service – Global Energy Transition Outlook (ETO)

Key supply sources in a delayed transition – the usual suspects

For oil, the Middle East and US Lower 48 are best positioned to ramp up supply, potentially meeting over 70% of the additional demand. The Middle East could supply more than 40% of the total liquids demand uplift, while North America would supply almost 30%. The remaining 30% would come from various regions, including Latin America and Africa's deepwater sectors.

For gas, nearly half of the additional supply would come as a by-product of heightened liquids-driven activity in North American tight oil plays, with dry gas plays in the US and conventional plays elsewhere making up the remainder.

Regional increment to base case (boe) Resource theme increment to base case (boe)

Source: Wood Mackenzie Oil Supply Model. Charts show combined impact on oil and gas supply.

The upstream supply chain would be stretched

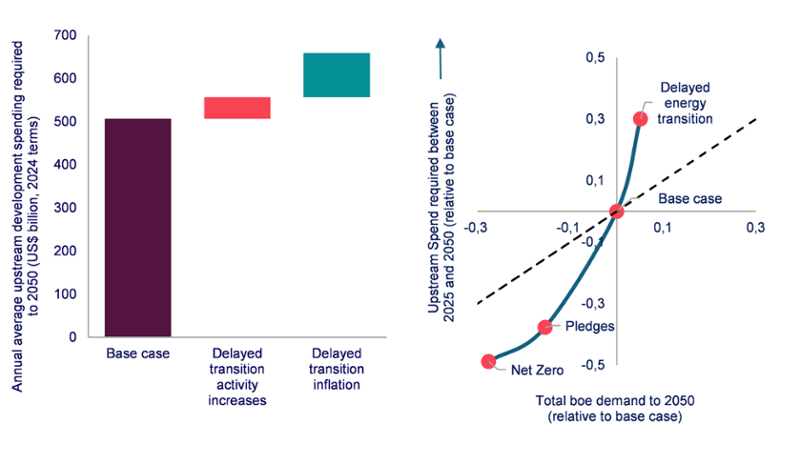

The global upstream supply chain, already operating near capacity, would face significant strain. There are four main inflation hotspots: North American onshore, Deepwater, the Middle East and LNG. Each would likely experience equipment and crew shortages, and disproportionately rising costs. The increase is not linear: 5% more demand would require 10% more activity, leading to 20% higher global unit development costs. This cost inflation would significantly impact project economics. For the 95 largest conventional undeveloped projects analysed, a 20% cost increase would raise breakeven prices by more than US$15/bbl at a 15% discount rate.

To meet the higher demand in a delayed transition scenario, upstream investment would need to rise by approximately 30%. This translates to average annual development spend of US$659 billion, versus US$507 billion to meet base case demand.

Incremental oil and gas supply costs The supply-cost relationship is non-Linear

Source: Wood Mackenzie Lens Upstream

Higher cost of supply would mean higher prices

In response to higher costs and demand under the Delayed Energy Transition, Wood Mackenzie's global Oil Supply Model forecasts Brent crude prices rising above US$100/bbl in the 2030s, before falling towards US$90/bbl by 2050. This represents an average increase of US$20/bbl barrel over the base case. The outcome is, of course, critically dependent on OPEC behaviour. The group could chase market share with more aggression or adopt more investment restraint than we assume. Either would have a substantial impact on prices.

To meet the investment requirements of a delayed transition, the oil and gas industry would need to evolve its approach to capital discipline. Key changes would include: raising return thresholds and breakeven targets; increasing corporate planning prices and potentially relaxing emissions intensity targets. Stakeholder support would be crucial for this shift. Higher oil prices could help build confidence, with US$100/bbl potentially generating US$6 trillion in additional government revenues and NOC equity value, plus US$1 trillion in increased corporate valuations for existing commercial assets (on an NPV10 basis).

Conclusion

A delayed transition scenario would have profound impacts on oil and gas company strategies:

- Oil-weighted companies, particularly Middle Eastern NOCs and US tight oil producers, would be well-positioned.

- Resource capture would become a priority, potentially driving M&A activity.

- Risk tolerance for larger, more complex projects could increase.

- Efficiency and discipline would remain important, with a focus on managing costs and emissions.

- Funding for oil and gas projects could become more accessible, though emissions reduction criteria would likely remain non-negotiable for many lenders.

The broader impact of higher oil and gas prices would include headwinds for the global economy, increased competitiveness for alternative energy sources and renewables, amongst many others.

The upstream sector has successfully adapted to meet supply challenges in the past. But a delayed energy transition would require significant investment and strategic shifts. The scenario underscores the complex interplay between energy demand, supply chain constraints, and climate goals, highlighting the need for careful planning and flexibility in the face of an uncertain energy

Fraser McKay, Head of Upstream Analysis, Wood Mackenzie and Angus Rodger, Head of Upstream Analysis for APAC the Middle East, Wood Mackenzie

This an excerpt from a longer paper, available to be download in full here Taking the strain: how upstream could meet the demands of a delayed energy transition | Wood Mackenzie