The Strait of Hormuz is no longer fully blocked for LNG tankers, with a handful of cargoes having been exported east from the Gulf. However, we do not yet expect a full restart of the lost LNG production from Qatar and the UAE that makes up around 20% of the world’s LNG capacity. The vital shipping route has never been entirely shut to traffic. Throughout the crisis that began with US strikes on Iran on 28 February, some vessels have made crossings of the strait. Iran, in particular, continued to export its oil through the strait until the US introduced their own military blockade further east.

For LNG, the closure was highly effective in the early weeks, but the situation has become more open in recent weeks. The first LNG tanker crossing of the Strait was Oman LNG’s ballast (empty) tanker the Sohar LNG, which left the strait in early April. Oman is one of the two countries bordering the strait.

In mid-April the UAE’s energy company ADNOC began LNG movements through the strait, with tankers turning off their signals and moving in secret. The Mubaraz left the Gulf with a cargo from the UAE’s Das Island plant around mid-April, heading east to Asia. Around the same time the Mraweh crossed west through the strait to pick up a cargo from Das Island, then crossed back east out again, later re-appearing on ship-tracking on a course to Japan.

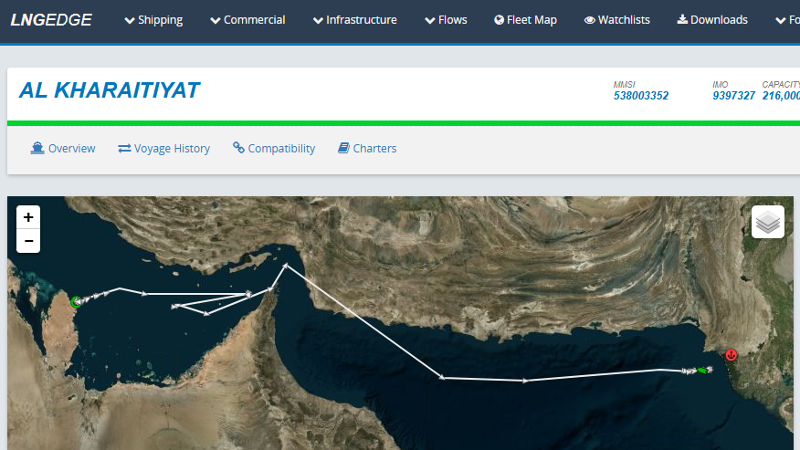

Map of the first Qatari voyage through the Hormuz

Source: ICIS LNG Edge

On Saturday 9 May a QatarEnergy ship crossed east through the strait for the first time: the Al Kharaitiyat, with a cargo for delivery to Pakistan. Qatar’s annual output is around 80 million tonnes/year, compared with 5 million tonnes/year for the UAE, so a restart of Qatari exports would be the most important change.

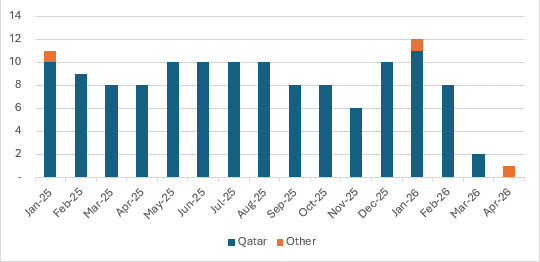

Pakistan normally imports around ten LNG cargoes per month, almost all of them from Qatar. While some countries, like Taiwan, have bought lots of cargoes in the spot market to replace their lost volumes from Qatar, Pakistan simply stopped taking LNG after the closure of Hormuz, only taking one single spot cargo. Pakistan likely struggled to pay the high spot prices for replacement cargoes. Instead it negotiated with Iran for a limited number of deliveries to be allowed through the strait for Pakistan. The country is also acting as a mediator between Iran and the US in peace talks, so was in regular communication with Iran.

Number of LNG cargoes to Pakistan by origin

Source: ICIS LNG Edge

So, there are special circumstances explaining the shipment to Pakistan, but we can’t yet say that the strait has re-opened to normal LNG traffic. The operators at Qatar’s Ras Laffan plant can’t fully restart production until they know they can export a regular flow of cargoes. LNG plants are big and complicated facilities, and can’t be turned on and off like a light switch. They can take days or weeks to start and shut down safely. So Qatar can’t fully restart just to produce a handful of cargoes.

There is some reliable demand within the Gulf itself. Kuwait imports around 7 million tonnes/year of LNG, mainly during the summer. There is also occasional demand from the UAE itself and from Bahrain. Qatar can supply this local demand, within the strait, without needing to be able to export through Hormuz. As there has been a fairly steady flow of cargoes to Kuwait in recent weeks it seems likely that Qatar has turned on some of its smaller production units to meet this local demand.

So, Qatar may be producing some limited volumes of LNG, and Qatar and the UAE have both exported a handful of cargoes through the strait. However, there is no sign yet of a resolution that would allow a full restart to take place and re-assure global gas markets. Around 7 million tonnes of LNG is lost to global markets every month that Qatar and the UAE are shut.

At the start of 2026, ICIS forecast that global supply would increase to 473 million tonnes for the year as a whole, up 31 million tonnes from 2025. A closure of four or five months would wipe out that increase.

The strait has already been mostly closed for two and a half months. Even if a peace deal was agreed tomorrow, it will still take a couple of weeks at minimum to restart all production. So most of the expected increase in supply this year has already been cancelled and if the outage goes on a few months more, 2026’s LNG output could be lower than 2025.

If there is a peace deal fairly soon, then gas prices could move a little lower, but the markets may make it through winter without too much additional difficulty.

However, if supplies remain short for more months, it limits Europe’s ability to refill gas storage ahead of winter and that could mean that there could be a danger of even higher price spikes to come in the winter ahead. The risk would be especially high if the winter is cold and Europe ends up having to compete for spare cargoes against richer Asian nations such as Japan, South Korea and Taiwan. So although the strait has partly re-opened, the crisis is far from over yet.