The oil market in 2022 saw unusual volatility—even by the standards of what is historically a very volatile commodity. What factors drove that volatility, and what are the prospects for the year ahead?

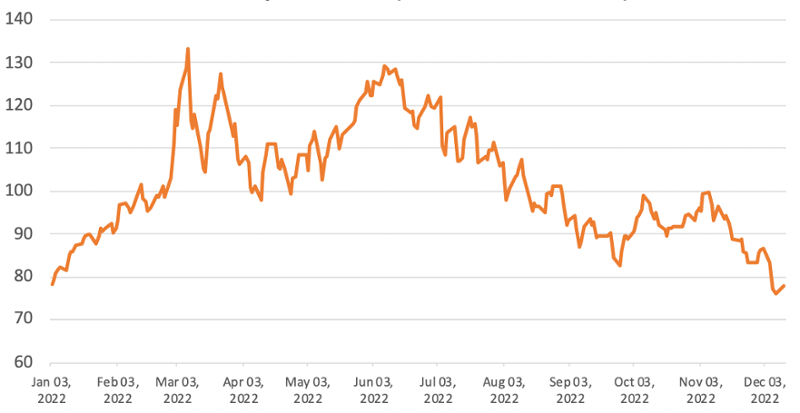

Even before Russia invaded Ukraine, global oil prices were in the midst of a strong post-COVID recovery. Oil prices entered the year near $80 per barrel. Recovering global demand combined with relatively tight supply—the result of OPEC+ production restraint and cautious investment by US shale operators—left global inventories very low.

The Russian invasion of Ukraine, and concern that Russian exports of crude oil and refined products would be disrupted, drove prices sharply higher, with the global benchmark crude Dated Brent reaching a peak of $133/bbl in early March. Even as it became apparent that the disruption to Russian supplies was not significant, prices remained above $100/bbl through much of the Spring and Summer. (After an initial dip because European companies scaled back purchases, Russian supply recovered as new buyers—especially in India and China—stepped in, although they were able to win large discounts of up to $30/bbl.)

Brent Dated Trend in 2022 (in $/b)

Source: EIA DOE

At the same time, global oil supply accelerated. For much of the year, the OPEC+ group maintained its policy of gradually unwinding the large production cuts put in place during the pandemic. And while US shale investors remained cautious, increased drilling led by privately-held companies helped boost supply by an additional 1 million b/d. In addition, the crisis sparked members of the IEA to engage in a coordinated release of roughly 250 million barrels from strategic oil stockpiles during 2022.

The combination of weaker demand and rising supply helped the global oil market move from a deficit to a surplus, and as inventories began to increase, oil prices declined. Even with renewed production cuts by the OPEC+ group (with a 2 Mb/d reduction implemented in November), oil prices continued to fall.

Indeed, the imposition of a nearly-full embargo by the EU on crude oil purchases from Russia in early December—and the imposition of a G7 price cap on Russia oil exports—failed to move markets, which reached a low-point of $76/bbl by mid-December amid ongoing demand fears.

Where will the market head in 2023? Of course the oil price is unpredictable, but here are the factors I will be watching closely:

- The EU is scheduled to implement an embargo on Russian refined products on February 5th, to be accompanied by a G7 price cap. Before the crisis, Russia was the world’s 2nd-largest refined product exporter (after the United States). Will markets for gasoline and diesel fuel react as smoothly as crude oil did to these policy moves? Will insurance and tanker markets be as flexible for refined products as they have been for crude oil?

- In a similar vein, how will Russia respond? Russian officials say they will not sell oil under the G7 price cap; in turn, G7 officials appear to have set the crude oil cap at a level that will not materially impact Russian revenues. How will this delicate dance play out in 2023?

- Will the OPEC+ group remain proactive in defending oil prices? Oil prices were about $90/bbl when the group announced its large 2 Mb/d cut a few months ago. While the group is currently not slated to meet until June, OPEC officials have said they could meet sooner—and agree on additional production cuts—if markets deteriorate further.

- Will demand remain weak as the US and European economies face a potential recession? How long will China’s oil demand remain weak due to COVID-related closures?

Oil remains by far the world’s largest energy source. The sharp increase in oil prices in 2022, and the re-emergence of geopolitical concerns, reminded consumers – and governments – around the world that oil remains a critical commodity. Even as we seek a rapid transition to a Net Zero future, 2023 is likely to see a continued focus on oil’s affordability and security.